It was back in November 2009 when Marc Faber of the Gloom, Boom & Doom Report made the call that gold would never go below $1,000 an ounce ever again. So far, he has been correct. I believe something similar can be said of oil today. Not that I’m calling a bottom just yet, but once oil breaks back through $60, I don’t think oil will fall back below it ever again. Too bold a call? Maybe, but here are my reasons.

Iran and Venezuela Not Coming Back Anytime Soon

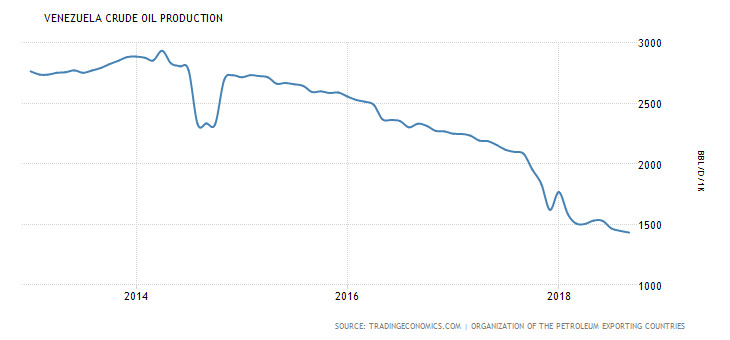

First, we have supply severely reduced from Iran and Venezuela. Historically, Venezuela has produced as high as 3.45 million barrels a month, a high hit in 1997. Before the oil crash of 2014, it was pumping about 2.5 million a day, and ever since the country’s collapse, that figure has gone down steadily, now to 1.43 million, a day and will likely fall further as the society there unfortunately continues to deteriorate.

The country’s idea for its oil-backed cryptocurrency, the Petro, as an OPEC standard to save its economy can barely be called half-baked. Socialist controls have not let up, nor will they without some sort of coup or revolution, which would temporarily disrupt current oil exports even more severely. As for Iran, before the nuclear deal, exports reached a low of 3 million barrels a day.

As of September, exports were at 3.76 million a day, so we have about another 760,000 barrels a day to fall. Taken together, I estimate that for these two countries, we will see a combined fall of 1 million barrels a day by Q1 of next year.

This month, foreign portfolio investors have sold Indian stocks and bonds the most in two years after a declining rupee made US assets more attractive, and rising global interest rates rendered the carry trade unviable.

Total bond and stock net sales by overseas funds touched a high of Rs 31,984 crore so far this month, show data from National Securities Depository.

Exits may quicken towards the year-end as funds compute performance bonuses for the year, dealers said. They sold a net of Rs 19,810 crore in equities, the largest monthly quantum this year. Debt sales amounted to Rs 12,167 crore.

“There is a flight to safety amid the improving US economy and rising global rates,” said Ashutosh Khajuria, CFO, Federal Bank. “Pressure has been mounting on the emerging markets. If India demonstrates better performance on macroeconomic indicators like iinflation, current account and fiscal deficit, those investors would come back again.”

This year, overseas investors have net sold Rs 93,481 crore of financial assets in India, the highest ever sale at least since 2002, data showed.

US unemployment, a key economic metric for the world’s biggest economy, fell to levels last seen about five decades ago, signaling a strong labour market and rising wages. That would mean the US policymakers would continue to raise headline lending rates.

“Rising US yields along with improving global economies have triggered investment exits from emerging markets,” said Sanjiv Bhasin, Executive VP-Markets, IIFL Securities. Softer oil prices and a stable rupee should reverse the market trend, he said.

“The debt market is going through uncertainties in the non-banking sector. Once it is settled, investors should regain confidence,” Bhasin said.

Two weeks ago, the US benchmark yield climbed to 3.23%, its highest level since May 2011. High US yields are prompting dollar funds to return to US assets that carry no currency risks.

Emerging market currencies have turned volatile, risking global investors’ investment returns on respective currencies. The rupee hit a record low of 74.48 per dollar and is one of the worst performing emerging market currencies.

The central bank did not raise the benchmark rate in its October bi-monthly monetary policy.

According to Marc Faber, a global market guru, tight monetary policies are good for the rupee, but not so good for the stock market.

It is different walking into the office. As it was in February. “How many points was Wall Street down,” a colleague says as he walks in this week. That morning the Dow Jones was down 127. The assumption that markets will fall instead of rise is a rare state of mind in the broking world, it only happens in a bear market. Of course nobody knows if a bear market has started, but the fact we are discussing it is a sign. The 7.8 per cent fall in the market is another.

Those that declare a bear market are reckless to do so, their hollow predictions no matter how confident and no matter how eloquently expressed, are little more than attention-grabbing guesswork, and somewhat irresponsible. But financial market commentators know that "calling the crash", no matter how unfounded, attracts attention. It gets hits to run against the herd and invoke fear, it gets hits to suggest everything is going to hell, so someone will always want to do it.

Despite that, an independent, agenda-less viewpoint, delivered without fear, is always interesting and of value, even when wrong. This is how commentators like Marc Faber and Nouriel Roubini have survived for so long despite being so repetitively wrong, because they are independent, free speakers and, of course, just occasionally, when the market tips over, they can claim the high ground and shout “I told you so”. Someone has to sit at the bearish end of the market’s bell curve of opinion and someone has to provide the devil’s viewpoint. It is a good space to occupy because there are not a lot of people there, so you stand out more easily.

But you can’t sit there if you’re trying to sell a financial product in the finance industry. Boom sells, not gloom and doom, meaning that financial market negativity is for people selling subscriptions not financial products. Which is why the bears are in the minority, because it serves nobody’s commercial purpose unless you are selling a newsletter that gorges on fear.

But this week, one of the major brokers, an institution permanently prone to optimism for commercial purposes, crossed the line. The mainstream getting bearish is another sign, when the institutions that are commercially biased to promote greed, move towards fear.

This week, Morgan Stanley’s chief US equity strategist wrote that the market is in the midst of a “rolling bear market” across all global risk assets caused by the drain in liquidity (the end of quantitative easing) and peaking growth (ending of the Trump tax sugar hit for corporate earnings). He says “with growth, tech and discretionary stocks, having now begun to underperform, the S&P 500, the final holdout of the ‘rolling bear market’, will eventually succumb, and probably soon”. The implication is that “the rebound last week was nothing but a dead cat bounce and the correction is not done yet”.

In times of flux, when volatility is high and everybody fears what will happen next, the herd can obsess over the irrelevant. It is doing so at the moment. The focus is on the S&P500, which has dropped below the 200-day moving average (again). Morgan Stanley says, “we look for confirmation [of a bear market] with a definitive break of the S&P 500 through its 200-day moving average”. Below the 200-day moving average is another sign.

Another bear market indicator is something called the Hindenburg Omen. It is a technical indicator that compares the number of 52-week highs to the number of 52-week lows on the New York Stock Exchange and purports to predict the likelihood of a market crash. It was named after Germany’s Hindenburg airship, which crashed in 1937. The Hindenberg Omen Indicator was developed by a chap called Jim Miekka, a blind mathematician, based on a series of criteria. All the criteria for a Hindenburg Omen were met on September 11 this year by the New York Stock Exchange.

Does it matter? Not really. The Hindenburg Omen is not a great indicator, it has a record of false alarms, but more interestingly perhaps is the fact it always triggers before any major market sell-off as it did in 1987 and 2008. Not every Hindenburg Omen signals a market top, but every market top sees the Hindenburg Omen triggered. It is another sign.

The Indian currency breached the 74-mark for the first time ever against the US dollar this month, but the worst could still be yet to come for the rupee.

Financial analysts are now wondering how low the rupee will continue to sink, as investors recoil over a significant amount of their gains in India being wiped out.

He claimed the rupee could record levels of up to 80 against the US dollar within just as little as six months.

Speaking to finance website MoneyControl, he said: “My own sense is that in the next 6 months, the rupee should stabilise between 72-74.

“However, in between, a spike towards 79-80 may happen.”

The Reserve Bank of India went against predictions from financial analysts as it held interest rates at the start of October.

The RBI's monetary policy committee (MPC) left the repo rate unchanged at 6.50 percent, with five out of six panel members voting to hold the rate

In its policy statement, the bank said: “Global headwinds in the form of escalating trade tensions, volatile and rising oil prices, and tightening of global financial conditions pose substantial risks to the growth and inflation outlook.”

Defending the decision, the bank said it was acting "to further strengthen domestic macroeconomic fundamentals”.

Marc Faber, veteran investor and publisher of the Gloom Boom & Doom Report newsletter, called on India to raise interest rates “meaningfully” to give the rupee some breathing space.

He said: “Either India has to increase interest rates meaningfully, which would mean that the economy would be hurt, or they obviously will have a weaker currency over time – and nobody can deny the fact that over the last 10, 20, 30 years, the rupee has been a weak currency.”

Earlier this week saw the Prime Minister of India issue a desperate call to oil producers to review payment terms to help ease concerns of soaring oil prices.

Oil prices have reached four-year peaks as the market focused on upcoming US sanctions on Iran while shrugging off the year's largest weekly build in US crude stockpiles.

India currently imports more than 80 percent of its oil needs.

Marc Faber, editor and publisher of 'The Gloom, Boom & Doom Report', who in an interview to ET Now earlier this year had projected a 20 per cent drop in Sensex to a sub-30,000 level, now says the rupee could hit 100 a dollar mark in the next few years.

India’s fiscal position is not particularly good. Either India has to increase interest rate meaningfully or has to let rupee depreciate over time.

Many international investors consider “real returns” a key gauge for emerging market investments.

Although there are multiple metrics to determine real returns, one popular mode is the difference between one-year government Treasury Bills and one-year projected retail inflation.

“With no further rate increase, the lure of India's real return may have diminished, especially when US Treasury is rising,” said Anindya Banerjee at Kotak Securities. “It would impact investor sentiment when the world is in a risk-off mode.”

The central bank did not raise the benchmark rate in its October bi-monthly monetary policy.

According to Marc Faber, a global market guru, tight monetary policies are good for the rupee, but not so good for the stock market.

This month, foreign portfolio investors have sold Indian stocks and bonds the most in two years after a declining rupee made US assets more attractive, and rising global interest rates rendered the carry trade unviable.

Total bond and stock net sales by overseas funds touched a high of Rs 31,984 crore so far this month, show data from National Securities Depository.

“There is a flight to safety amid the improving US economy and rising global rates,” said Ashutosh Khajuria, CFO, Federal Bank. “Pressure has been mounting on the emerging markets. If India demonstrates better performance on macroeconomic indicators like inflation, current account and fiscal deficit, those investors would come back again.”

This year, overseas investors have net sold Rs 93,481 crore of financial assets in India, the highest ever sale at least since 2002, data showed.

US unemployment, a key economic metric for the world’s biggest economy, fell to levels last seen about five decades ago, signaling a strong labour market and rising wages. That would mean the US policymakers would continue to raise headline lending rates.

“Rising US yields along with improving global economies have triggered investment exits from emerging markets,” said Sanjiv Bhasin, Executive VP-Markets, IIFL Securities. Softer oil prices and a stable rupee should reverse the market trend, he said.

“The debt market is going through uncertainties in the non-banking sector. Once it is settled, investors should regain confidence,” Bhasin said.

Two weeks ago, the US benchmark yield climbed to 3.23%, its highest level since May 2011. High US yields are prompting dollar funds to return to US assets that carry no currency risks...

Dr. Marc Faber, editor of the Gloom, Boom & Doom Report, spoke on SBTV about the state of the global financial system. Despite the trade wars initiated by the Trump Administration, the U.S will be unable to compete with Asia to reverse its trade deficit. Dr. Faber believes that the US cannot be competitive even if there is free trade.

Compared to the 70s, the stock market now is a significant part of the US economy. A stock market crash will have a huge impact on the economy today, probably enough to trigger a depression. In general, many assets are expensive today due to monetary inflation.

The Bank of Japan is now a major shareholder in nearly 40% of listed companies in Japan as the central bank keeps buying stocks under its ultra-loose monetary policy. If such central bank interventions become pervasive, Dr. Faber thinks it is possible for a central bank to own most of the assets in a country. This would be tantamount to achieving silent socialism.

THE India rupee could plunge to depths of 100 against the US dollar if the crisis-hit currency continues to fall in value against the US dollar, according to a prominent investor and economic analyst known as ‘Dr Doom’. The languishing rupee has shed around 15 percent of its worth versus the American currency this year and is currently the worst-performing tender in Asia.

This month saw the rupee breach the 74-mark for the first time ever against the US dollar as it falters under pressure from soaring oil prices and higher interest rates.

Financial analysts are now wondering how low the rupee will continue to sink, with Marc Faber, veteran investor and publisher of the Gloom Boom & Doom Report newsletter, admitting that “India’s fiscal position is not particularly good”.

As of just before 12:30 BST, the Indian rupee is trading at 73.61, according to data from Bloomberg.

When asked if the rupee could plummet to levels of 100 against the US dollar, Mr Faber said this would require a depreciation of 5 to 10 percent per year.

But he stressed that this process would need to rumble on for “the next few years” in order to reach triple figures against the greenback.

Mr Faber told The Economic Times: “Well the timeframe is I would look for is a depreciation of 5 to 10 percent per year for the next few years.”

Mr Faber also called on India to raise interest rates “meaningfully” to give the rupee some breathing space.

He said: “Either India has to increase interest rates meaningfully, which would mean that the economy would be hurt, or they obviously will have a weaker currency over time – and nobody can deny the fact that over the last 10, 20, 30 years, the rupee has been a weak currency.”

The Reserve Bank of India went against predictions from financial analysts as it held interest rates at the start of October.

The RBI's monetary policy committee (MPC) left the repo rate unchanged at 6.50 percent, with five out of six panel members voting to hold the rate

In its policy statement, the bank said: “Global headwinds in the form of escalating trade tensions, volatile and rising oil prices, and tightening of global financial conditions pose substantial risks to the growth and inflation outlook.”

Defending the decision, the bank said it was acting "to further strengthen domestic macroeconomic fundamentals”.

What is happening with the EM currencies? The fall also reflects the gain in the trade weighted dollar index pegged towards EM currency basket. Is the dollar buying seen as risk aversion or just better yield?

It is the question more of this tightening global liquidity and the way emerging economies borrowed. They borrowed in dollars and so there is a lot of demand for dollars to pay the interest on the dollar debts.

Number two, when you look at international investors, they have some cash and they have some bonds. If you look at what they do in terms of money in cash and in bonds, they can buy US treasuries. The 10-years now are available at an yield of 3% but they could also buy in Europe treasuries but the yield would be much lower.

For example, in Germany they would get a yield of 0.5% on German governments. In Portugal, they would get 2.2%, in Spain 1.66%. The dollar compared to this European currencies and bonds is relatively attractive in terms of a yield. It is not particularly attractive as a currency because some emerging economies have a much better financial condition today than they had in the last crisis or in ‘97-98.

If you ask me what I think about India, last time I said the currency has become a bit oversold and may rally a little bit, maybe to 71-72 against the US dollar. But I think the long-term trend of the Indian rupee is down...

What are rising yields across US as well as Europe indicating about the risk that the world is running on?

The financial markets were already very fragile at the beginning of this year and this fragility has actually increased because there is a tendency among central banks to step back from asset purchases, letting interest rates gradually adjust on the upside. And so this liquidity that we have in the world has been diminishing. It is not shrinking, but it is growing at the diminishing rate.

Then came the announcement of the Trump administration. It is a really bad idea to pick on China and to launch not only a trade war but a confrontation with the US’ largest trading partner who also happens to be a large buyer of US assets, bonds, stocks and of course, properties.

This idea has disturbed the financial markets around the world and so they are adjusting on the downside. Now, I would not call that the crash. A crash happened in 1987 when the Dow Jones dropped 21% in just one day.

In the US, we have gone from a peak to the current level, down by 7%. This is nothing. This is after an increase of the S&P from 666 in 2009 to the current level of over 2900. This correction is really not very meaningful but yet it may become meaningful.

SBTV’s latest guest is Dr Marc Faber, editor of the Gloom, Boom & Doom Report. We discuss the signs showing that the US is an empire in decline and how the next financial crisis will impact asset owners. Despite the video difficulties in this episode, Dr. Faber doesn’t disappoint and delivers a great interview on various topics.

We also asked Dr Faber what he would do to reverse the US trade deficit if he was the President of the US.

There’s always market pessimists to tell you “I told you so.”

‘Permabear’ is a term used for pundits like Societe Generale’s Albert Edwards or newsletter writer Marc Faber who predict market calamity on a weekly or monthly basis without respect to recent market activity.

Permabears are really only the tip of the iceberg, though. The number of pundits who are pessimistic 60 or 80 per cent of the time is far larger than the count of devout permabears.

The end result is that there is never a shortage of dramatic calls for catastrophe so when anything truly bad happens in markets, business TV will find someone to gloatingly announce: “I told you so, but you wouldn’t listen.”

“To state the obvious: for every buyer there must be a seller. Wild views about future market events, long or short, should be treated with the same scrutiny. Claims that Tesla is going to $4,000, or the Fed’s quantitative easing program is going to cause hyper-inflation, should be judged on their merits, not on the extent to which they tap into fears over another crisis… Brave, contrarian predictions are supposed to lean against the kind of herd mentality that drives exuberant valuations. Think Templeton during the Nasdaq bubble for instance. But perhaps the bubble is now in predicting the next systemic crisis, rather than assuming everything will be OK.”

As Alphaville points out, this doesn’t mean investors can always ignore pessimism. New short positions put in place by famed fund manager JimChanos, for example, are always worth further research. It is a key point that Mr. Chanos has been correctly bearish numerous times on many short trades, not just once. As a foreign exchange trader once told me, “It’s easy to be bearish, you have to be bearish and make money.”

Mounting US pressure on Turkey is hardly a good diplomatic strategy for Washington and its allies, says veteran investor Marc Faber. Ankara has other countries to make alliances with.

“[US President Donald] Trump doesn’t pursue foreign diplomacy. He is just like an elephant in a porcelain shop. He picks on this, picks on that, but there is no diplomacy at all,” Faber told Turkey’s Anadolu news agency.

Turkey has some leverage regarding the recent tension between Washington and Ankara, he said. “This is the Trump card that Turkey have – NATO. NATO has significant bases in Turkey. In the long run basically Turkey has two options; it can be closer to Europe and stay in NATO, or it could join the Shanghai cooperation.”

“That would imply that Turkey abandoned or have less relationships with the West and more relationships with Russia and China. This is a possibility that [Turkish President Recep Tayyip] Erdogan has. I think Trump doesn’t realize that this option is very realistic.”

Faber noted that after the harsh sell-off that hit the Turkish markets, now is a good time to invest in the country. “People always say they would like to buy low and sell high. Turkish stocks are valued in US dollars. Now it’s in buying range. I think I will buy some Turkish stocks, ETF’s [Exchange Traded Funds]. I own some [Turkish] bonds. It’s not the huge portion of my portfolio but yes I own some Turkish debts. I think it’s the time to buy Turkish assets,” Faber said.

The Turkish economy has recently been hit by a record depreciation of the national currency – the lira. On Friday, Trump doubled tariffs on aluminum and steel from Turkey in response to the detention of a US citizen. American pastor Andrew Brunson is being held on terrorism charges in Turkey, facing up to 35 years in prison for his alleged role in a failed coup in 2016.

In response, Erdogan announced a boycott of US electronic devices, including Apple iPhones. Turkey has also hiked tariffs on US goods such as tobacco, alcohol, cars, cosmetics and others.

Renowned global investor and markets commentator Marc Faber, best known for being a market pessimist which earned him the nickname "Dr. Doom", said Wednesday Turkish assets could present a good investment opportunity at the moment.

Although the economic strategist has been warning since 2010 that global markets are headed for a 1987-style market crash, Faber told Anadolu Agency (AA) in a phone interview that he didn't foresee such a grim future for the Turkish economy.

"People always say they would like to buy low and sell high. Well, Turkish stocks are valued in U.S dollars. At the moment they are within buying range. I am going to buy some Turkish assets, ETF's (Exchange-Traded Funds)," he said.

Stating that he already had some Turkish bonds, although not in very large quantities, Faber said now was a good time to invest in Turkish assets.

Faber, who is also the publisher of "The Gloom, Boom & Doom Report", said Turkey must reduce its sensitivities, narrow its trade deficit and close its current account deficit to not be affected by volatility in the coming period.

Reiterating that the foreign and economic policies of the United States were not right, the Swiss investor said: "Trump is not pursuing diplomacy in foreign policy. He is like a bull in a china shop. He keeps picking on everyone; there is no diplomacy whatsoever. "

"Turkey's Trump card is NATO. NATO has crucial bases in Turkey. Turkey has two options in the long-term; it can stay close to Europe and stay in NATO or join the Shanghai Cooperation Organization. This would indicate that Turkey has left the West or that it will be in less contact with it, becoming closer with Russia and China instead. This is an option in Mr. Erdoğan's hand. I think Trump does not understand that this is a very real possibility," he said adding that Turkey was not without alternatives.

Underlining that U.S. President Donald Trump's trade policies could drag the world into recession, Faber said, "Economists around Trump believe that imports from China are responsible for the U.S.' trade deficit. China is the indicator of the US.' declining competitive power. The U.S. has had low capital investment over the last 20-30years. Economists believed that consumption should be increased to increase growth. The result is naturally an increase in trade deficit. "

Faber pointed out that the consequences of the global trade wars initiated by the U.S. could be devastating, saying "Trade wars are complete madness. They are continuing at a time the global economy is already slowing down. Just look at copper prices now, for example, they have completely collapsed. This is a sign that the global economy is slowing down. I think we are headed towards a recession."

President Trump announced on Aug. 10 that the U.S. was doubling aluminum and steel import tariffs on Turkey, fixing them at 20 percent and 50 percent, respectively.

In retaliation, Turkey also increased tariffs on several U.S.-origin products, including alcohol and tobacco products and cars, according to a new presidential decree published early Wednesday in the official gazette.

Dr. Marc Faber was born in Zurich, Switzerland and obtained a PhD in Economics at the University of Zurich. Between 1970 and 1978, Dr. Faber worked for White Weld & Company Limited in New York, Zurich and Hong Kong. From 1978 to February 1990, he was the Managing Director of Drexel Burnham Lambert (HK) Ltd. In 1990, he set up his own business.

US influence on the global economy has been gradually falling, and emerging economies like China and India can overtake the US as global leaders, according to Marc Faber, editor and publisher of The Gloom, Boom & Doom Report.

“The US as an empire against the rest of the world peaked in 1950s or 1960s. Then, there have been other countries that have become more powerful, in particular China and now increasingly India. The US empire and its influence on the world is diminishing and has been diminishing for quite some time,” he told RT. The trade war may accelerate this “mutation” in the global economic balance “with other countries becoming more important and the US less important,”Faber said.

According to Faber, the US is likely to be the biggest loser from the trade war it started. “The winners in a real trade war would be everyone except the US. The Europeans would trade more with Asia, and the Asians would trade more with Europe than the US. There would be more trade between the emerging economies and China and vice versa,” Faber said.

Another winner from the trade would be Russia since China would buy more resources from the country, while Moscow would buy more from Beijing, he said.

The US stock market has thus far ignored the news about the global trade war, Faber notes. “But if there is trade war, it is not good for the global economic growth. The global economy is slowing down already. I think it would be a big mistake to go ahead with the trade war.”

The countries most exposed to the trade war in emerging markets are Brazil, Turkey, and Argentina, due to their fiscal problems, growing deficits, and weak currencies amid large amounts of foreign debt, Faber said.

With the global economy financed by soaring debt since the last global crisis of 2008-2009 another recession is likely to come, but its shape is not yet known, according to the investor.

Despite the recent strength of the US dollar, especially against the currencies of emerging economies, Faber says the trend will not continue in the long run. He says the best way to protect individual investments in times of turmoil is to diversify the portfolio with cash, bonds, precious metals, and real estate.

Marc Faber, editor and publisher of The Gloom, Boom & Doom Report, said he would not be surprised if Indian markets corrected 20% from current levels, but did not give a timeline for such a correction. In a phone interview from Chiang Mai, Thailand, the Swiss investor expressed concerns over the trade war, and said it is not beneficial to anyone.

What do you think could be the repercussions of global trade war on the world economy and markets?

There is less or hardly any growth in Europe. The Chinese economy has been slowing down, as well as other Asian economies. The US stock market by any measure is highly priced.

We have recessions in Argentina, Brazil and Turkey. We have currency weaknesses around the globe in dollar terms, which is a sign of monetary tightening, and now we have also this so-called trade war. Some people may suffer more, and some less but a trade war cannot be beneficial for anyone. In general, it is not a positive for the global economy or the financial markets.

Indian markets recorded new high today (Thursday). Do you think the rally in India is sustainable or do you think there is a correction in the offing for benchmark equity indices?

When (Indian) market hit a high earlier this year in January, my sense was that high would be an important one, but we made a new high.

Let’s put it this way, when I travel around the world and I visit financial institutions, first time India is really a subject. For the first time, investors think that India has an experience and a meaningful fundamental improvement due to the Modi government. They are not sure if it is the right time to invest now in India. Over the next 10 years, we want to have some money in India, regardless.

If you look at the S&P (500), and Indian stock market over the next 10 years, you will make more money in India than American shares. This has been my view for the last three years, and this remains my view.

Of course, if the global stock markets are going down— all the major markets, except India are going down. When everything is weak, and India is still strong, I will be reluctant to buy the market which is strong. It (rally) may last a little bit longer but it doesn’t mean it is good value. Valuations are not attractive other than a few exceptions.

How do you see it faring from here?

The bull market in India started in late 2015, We have seen a big move, I wouldn’t be surprised if there is a 20% correction. I cannot give you a date though.

If you put all your money now in Indian stocks, the reward in my opinion will not be great, as there are internal and external risks.

It's unfortunate that "hate speech" arbitrarily defined and dictated by the left is suppressing free speech and the search for objective truth. "Thank God white people populated America," uttered by Marc might have been said in a less offensive manner, but to remove the truth-seeking thoughts of a freedom-loving, non-racist intellectual of Dr. Faber's stature is unconscionable and ultimately destructive, most of all to minorities.

We are delighted to have Dr. Faber with us to discuss the global markets as he once did on all major business channels, at Barron's, and other mainstream print media. We ask Marc about Trump's economic policies, global monetary policy, stocks, bonds and precious metals, geopolitics, dollar hegemony, the Petro yuan, and much more.

Eric King: “I know you’ve had some issues coming into the United States, where you’ve been in an airport where they have taken you to the side and put you in a room (Dr. Faber laughs), which seems preposterous. But this move to more of a police state in the West, does that have you concerned?”

Dr. Marc Faber: “Well, that is another possibility, that we go more to a fascist regime rather than to socialism. That is a possibility that we need to entertain. And it is very clear to me, having grown up in the 1950s and 1960s, that today there is much more control of what you and I do. It’s stricter and more unpleasant…

We have far more regulations, far more laws, that actually are very negative for the small businessman, from which actually the economy grows the most. That also has a negative impact on growth. I would say whatever scenario you look at, the only scenario that could boost growth, briefly, substantially, would be war.”

A big difference between the market today and that of the 1987 crash is unfunded pensions. Renowned investor Dr. Marc Faber, who holds a PhD in economics, says, “The unfunded liabilities have gone up. They did not go down...

Marc Faber gives his up to date investment advice and discusses the current markets he is interested in most. Overall, he sees Asian markets as a safer place for your money, over Western markets.

"The rupee will be at these levels, maybe a rupee here or there. I don’t see rupee going to 75-76 to the dollar and there is no reason why it should. We have $400 billion of reserves and we are the most investible country.

We have never had any defaults, our track record is tremendous compared to other emerging markets and our levels of debt are nothing as compared to China. So on all those parameters, I think India is doing well and will do well.

Always remember, Marc Faber, one of the gurus of emerging markets, he always said one thing, the locals know best."

One of the staggering developments from the mad money world of stock markets is that US stocks rose overnight, with the Dow Jones index up over 180 points, as the deadline to President Trump’s trade war looms today. And what’s even more surprising is that some professionals reckon the market has priced in the effects of a trade war!

Gee I hope they’re right, but I don’t know how I or anyone could really test that.

This confidence that market experts know what lies ahead was captured by this from Jeremy Klein, chief market strategist at FBN Securities: “Any news we get on trade in the short term will be neutral or good,” he said. “We already know all the bad news that's out there on this issue.” (CNBC)

What he’s saying is that experts on the significant companies affected by a tit-for-tat trade war have worked out the profit effects of tariffs and then changed their valuation on that company. But those calculations operate off assumptions that might end up being wrong!

This is how the trade war should begin, with a U.S. Trade Representative statement saying tariffs on $34 billion of Chinese goods will take effect at 12:01 a.m. in Washington. Then China will return fire immediately. The assumption is that China will hit back with equal force. But what if they don’t, instead hitting harder than expected and on industries that were not expected to be affected?

All’s fair in love and war. And you can’t expect that a trade war will be fought out following some gentlemanly rules of engagement. Mind you, I hope it is, and I also hope the market experts have calculated the effects accurately. But I always argue that hope is not a strategy upon which you can build wealth in the stock market!

What worries me about this complacency on the trade war is that it comes when the doomsday drones are ganging up to ramp their warnings about an imminent recession and stock market sell off.

You shouldn’t be surprised about this, as since the end of the GFC this mob has tipped a Great Depression, countless market crashes and some have even had the Dow Jones plummeting below 10,000 while it’s now over 24,300!

Donald Trump has been seen as the trigger, with this one from Bloomberg showing how the negative nervous Nellies have been scaring us for some time: "Citigroup: A Trump Victory in November Could Cause a Global Recession!" (Bloomberg Financial News headline, August 2016)

And then this one: "A President Trump Could Destroy the World Economy!” (Washington Post editorial, October 2016).

Then there have been the likes of Harry Dent and Marc Faber who have been tipping a market Armageddon for at least three years, probably longer. These guys will get it right one day, after being wrong for a long time. And this trade war could be the trigger for them being free to boast about their insights.

All this comes at a time when investor surveys show that those playing the stock market are losing confidence. And some well-known fund managers have expressed their concerns about being long stocks, with the likes of Bridgewater Associates’ Ray Dalio saying he’s getting out of financial assets.

“It’s a classical late cycle story. So, when I was here last time, I said we were long and nervous. We are no longer long, we are increasingly nervous about this,” Roelof Salomons, chief strategist at Kempen Capital Management, told CNBC’s “Squawk Box Europe” on Thursday.

A late cycle represents an economy that has been growing, but is poised to fall into a recession, amid rising interest rates, lower profit margins and other negative economic headwinds.

And a trade war could be a cyclone, while the experts are treating it more like a zephyr. I’m gambling that these guys and their assessments are right because I think the current economic and corporate profitability stories are so strong. But I know I’m gambling.

If you can’t afford to gamble and see stock prices slide, then you might have to play it safer than me. But let’s all pray that this trade war doesn’t prove some Trump-haters right.

Dr. Marc Faber was born in Zurich, Switzerland and obtained a PhD in Economics at the University of Zurich. Between 1970 and 1978, Dr. Faber worked for White Weld & Company Limited in New York, Zurich and Hong Kong. From 1978 to February 1990, he was the Managing Director of Drexel Burnham Lambert (HK) Ltd. In 1990, he set up his own business, Marc Faber Limited which acts as an investment advisor and fund manager.

Dr. Faber publishes a widely read monthly investment newsletter, “The Gloom Boom & Doom Report,” which highlights unusual investment opportunities, and is the author of several books including Tomorrow’s Gold: Asia’s age of discovery which was a best seller on Amazon. Dr. Faber is known for his “contrarian” investment approach and charismatic personality. He became infamous after calling the 1987 crash in US equities.

Nomi Prins is an American author, journalist, and Senior Fellow at Demos. She has worked as a managing director at Goldman-Sachs and as a Senior Managing Director at Bear Stearns, as well as having worked as a senior strategist at Lehman Brothers and analyst at the Chase Manhattan Bank.

Prins is known for her books All the Presidents’ Bankers: The Hidden Alliances that Drive American Power and Collusion: How Central Bankers Rigged the World.

Renown Swiss investor and publisher of "The Gloom, Boom and Doom Report" Dr. Marc Faber discusses the global markets, housing and bond bubbles, central bank manipulation, gold, Trump, the petroyuan, the New Silk Road and what a potential conflict between the U.S. and China might look like as old empires die and new ones are born.

The U.S. stock market's latest run to all-time highs could be giving investors a false sense of security.

Market watcher Marc Faber, often hailed as the original "Dr. Doom," is not backing down from his long-held correction warning — even though nothing has materialized.

"You don't see, and I don't see. And, nobody sees. That's why people keep buying stocks. And yet, something will happen one day," the publisher of "The Gloom, Boom & Doom Report" said Tuesday on CNBC's "Futures Now."

He said several scenarios could trigger a deep correction.

"I think it may very well come from a credit event. Or, it may come from the disclosure of a major fraud. Or, it may come because interest rates start to go up," he said.

For now, it appears the rally isn't cracking. The S&P 500 has had 36 record closes this year. The Dow has done even better.

"In 2009 when stocks bottomed out, I can tell you that not many people saw why stocks would go up," Faber said. "Now it's the opposite. The sky is clear. Corporate profits have been expanding — they're good. Interest rates are low, but valuations are very high."

My co-host and I interview Dr. Marc Faber to discuss his views on the global economy, emerging markets, and the trade war.

An underlooked risk Marc mentions lies in the voting patterns of milennials.

Marc also tells us what his biggest trading mistake was and his unusual work schedule.

Marc Faber joins us as a special guest on this show, and it makes for a great conversation on markets, the economy, why the rent is too high in California, his advice for milennials, and his unusual sleep schedule. We also discuss the US-China trade negotiations, its impact on other emerging market economies, and what catalysts could possibly cause the market momentum to shift directions.

Marc Faber of The Gloom, Boom and Doom Report has some alarming things to say about how America’s foreign policies may have disastrous implications for the U.S. and global economies, and for the dollar.

He also weighs in on which asset class, crypto-currencies or precious metals, will ultimately will be the major benefactor of all of the pending geopolitical unrest. Don’t miss a tremendous interview with Dr Doom, Marc Faber, coming up after this week’s market update.

Marc Faber says the U.S. Dollar’s strength will not last long. “The last thing the U.S. administration wants today is to have a strong Dollar.”

Right now, investors are geared towards equities and cryptocurrencies. However, Faber expects within a few years investors will turn towards gold and silver. Faber does not have faith in most cryptocurrencies.

While he says blockchain technology is here to stay, he thinks the vast majority of cryptocurrencies will fail.

In this wide ranging interview, Jason asks Marc about asset price volatility, whether the stock market is topping, central bank balance sheets and whether they can be meaningfully reduced, the credit bubble in China, the US vs China trade war, and the popularity of crypto currencies in Asia.

With global markets struggling for direction after a rocky start to the year, Dr Doom has been conspicuously absent from the conversation. Investment adviser Marc Faber, 72, who adopted the nickname in 1987 after a newspaper column highlighted his contrarian outlook on markets, has had a quiet six months.

Faber – a once regular guest on business news shows such as CNBC’s Squawk Box and Bloomberg Television – has faded from view since the publication of his October newsletter The Gloom, Boom & Doom Report for comments that were condemned as racist. This included a passage where Faber used offensive racial references in laying out a bleak picture for the US if its early immigration flows had been from Africa rather than Europe. He has since been dropped from the booking lists for programmes at Fox News and CNBC, according to Reuters.

At the time, Faber told Canada’s Global & Mail he stood by the remarks, saying in an email exchange that he did not regret writing the passage and that he had a free right to express his views.

When This Week in Asia spoke to Faber at his suite at the Grand Hyatt in Hong Kong this year, he sounded resigned to the loss of his appearances on business television.

“Everything in life and the universe has a timeline, it is transient. In other words, what you have today, you may not have tomorrow,” Faber said.

Known for a keen interest in history, and the works of innovators such as Russian “wave theory” economist Nikolai Kondratiev, Faber has slipped from the public spotlight just as global markets have entered a period of heightened volatility...

The tariffs are going to backfire on the US very badly because you have to understand that the US was economically very powerful until the early 1980s. The same was the time in the 70s and early 80s. If America sneezes, Asia catches the cold because all the exports went to America. But this is no longer the case nowadays. Take steel. 2% of US steel imports are from China and only 1.5% of Chinese production of steel is exported to the US.

Even if the US would not buy any steel at all from China, it would not matter to the Chinese. At the time of Davos in February, a Chinese owner of the world’s largest bus company was interviewed and they asked him about US tariffs and chances of trade war with US. He said we really do not care. We export our buses to 150 different countries in the world, what do we care about the American market and that is true for many companies. The American market is no longer that relevant. China exports more to commodity producers than to the US and the same applies to the South Korea.

What has changed in the last 30-40 years is that whereas Asia and the world was American centric before, the world has become much more China centric in Asia and it is a much more multi-dimensional global economy where the US has lost a lot of its importance, relatively speaking. It has also lost the lot of prestige because of their failed interventions in Iraq, in Syria, in Libya, in Afghanistan, everything they touched, they messed up.

Marc Faber, editor and publisher of the Gloom, Boom & Doom Report joins BNN to discuss why U.S. President Trump's goal of 3-per-cent economic growth is unattainable.

In terms of interest rates, historically, our standards have been at the lowest level in the history of mankind from say 3000 BC up to now. So, in 5,000 years of history, we have never been this low. In the US, the low for the 10 years treasury was at 1.37% in July 2016 and in Europe, in many cases, there have been negative interest rates.

Recently, that has moved up a little bit but in Switzerland and in Japan, basically we still have negative interest rates and we have had them essentially for the last eight-nine years. This is a very unusual situation. I do not think anyone could expect interest rate to stay this low for much further. There is a rising tendency but recently the treasury bonds in the US have sold off quite considerably and I believe that we could have one more decline in interest rates as a result of a recession that may happen later on this year or next year. So, I actually went long on some treasury bonds in the US.

Concerning global trade, you are right. The idea was that multinationals in Europe and especially in the US could open up new markets like China and then sell their goods into these markets. But conditions have somewhat changed in the sense that it is the Chinese and other emerging economies that sold their goods into the US.

So to some extent, it backfired on the US and as you know the US is not the fair player and they reacted negatively. These trade sanctions or trade barriers, in my view are not very negative for China and other countries. Rather they are very negative for the US. This is my assessment of the situation.

Marc Faber, editor and publisher of the Gloom, Boom & Doom Report joins BNN to discuss why Canada needs to diversify its trade policy away from the U.S.

There is a lot of liquidity here in Asia. But offsetting that, there is also a lot of debt and the debt level in the world nowadays as a percent of the economy is more than 50% higher than it was in 2007 before the crisis occurred. We had this modest economic expansion since June 2009 but it was driven by money printing and credit and we have reached probably the level of credit where additional credit will not do much good.

India from a longer term point of view is still a good proposition but India is not exactly a problem-free country. There is leverage in the system and there has been fraud and there are still some unsettled political events that may happen.

I would say given that the market has actually rallied very strongly over the last few years and that we have reached a high at 36400 on January 29th , we could easily decline by around 20% from the highs that would take us below 30000. Long term, I am optimistic but we have to realise that if one asset class goes down, fund managers will also sell another one even though the fundamentals may be favourable but they just get out and build up their liquidity because on institutional side, the funds are holding very little liquidity. So, they may build up liquidity and that can then bring about selling pressure everywhere.

I do not think that dynamics have changed a lot. I still have a view that over the next 10 years, you will make more money in India than say in the US. In fact, looking at the various economies around Asia and the world, I would feel reasonably confident to say that India has a growth potential of say approximately 6% per annum which to Indians may not sound a lot but that is much better than the Europe and the US.

I do not think that this is a problem. The problem in India is more that Modi has some difficulties in reducing the still enormous bureaucracy. It may have improved somewhat but there’s still a lot of bureaucracy and there are still a lot of bad loans in the books of banks and then there is also the valuation issue. Blue chips in India sat at 40-50 times earnings. I do not consider that to be a low valuation. These factors could easily contribute to a big -- 20-30% disruption.

In an interview with ET Now, Marc Faber, The Gloom, Boom & Doom Report, says long term, he is optimistic about India but if one asset class goes down, fund managers will also sell another one even though the fundamentals may be favourable.

My guest in this interview is Dr Marc Faber. Dr. Faber was born in Zurich, Switzerland. He went to school in Geneva and Zurich and finished high school with the Matura.

He studied Economics at the University of Zurich and, at the age of 24, obtained a PhD in Economics magna cum laude. Between 1970 and 1978, Dr Faber worked for White Weld & Company Limited in New York, Zurich and Hong Kong.

Since 1973, he has lived in Hong Kong. From 1978 to February 1990, he was the Managing Director of Drexel Burnham Lambert (HK) Ltd. In June 1990, he set up his own business, MARC FABER LIMITED which acts as an investment advisor and fund manager.

I was expecting a correction a long time ago. It has not happened but when it happens, it happens in a more severe manner. So far, it has not happened very severely in the US. We are down not even 10% from the January 26 high. In India, we are down about 10% from the January 29 highs but it is not yet a big correction by historical standards. A correction would be a 20% decline and the bear market would be something like a 40% decline. It is nothing very serious yet but it may become very serious in the future.

I was expecting a correction a long time ago. It has not happened but when it happens, it happens in a more severe manner. So far, it has not happened very severely in the US. We are down not even 10% from the January 26 high. In India, we are down about 10% from the January 29 highs but it is not yet a big correction by historical standards. A correction would be a 20% decline and the bear market would be something like a 40% decline. It is nothing very serious yet but it may become very serious in future.

In terms of interest rates, historically, our standards have been at the lowest level in the history of mankind from say 3000 BC up to now. So, in 5,000 years of history, we have never been this low.

In the US, the low for the 10 years treasury was at 1.37% in July 2016 and in Europe, in many cases, there have been negative interest rates...

Watch this segment to know what famous Swiss investor Marc Faber has to say about India and its economy. In an exclusive interview to Zee Business today, famous Swiss investor Marc Faber said that the Sensex can still fall over 20 per cent, slipping below the 30,000 mark.

Renown Swiss investor and publisher of "The Gloom, Boom and Doom Report" Dr. Marc Faber discusses the global markets, housing and bond bubbles, central bank manipulation, gold, Trump, the petroyuan, the New Silk Road and what a potential conflict between the U.S. and China might look like as old empires die and new ones are born.

First interview up, Louis Navellier of Navellier & Associates notes that the best corporate earnings in 6 years and tax cuts could spur forward the already lofty US equities markets in 2018.

Dividend yielding stocks may be preferable in 2018, but caution is advisable before chasing high yields, which only magnifies risk / volatility.

The host / guest concur that NVIDIA (NVDA) shares are appealing, due in part to record demand for their superior crypto-mining GPUs, a top holding of our guest. Louis Navellier also holds UCTT, Ultra Clean Holdings, and Chinese stocks in anticipation of the Morgan Stanley Chinese stock index update, including the Twitter of China, WEBCO, ticker WB. Another key holding, Align Technologies, ALGN, maker of the popular dental tool, Invisalign is in his portfolio.

Outside of the equities markets, our guest is also adding copper and lithium contracts amid the auto battery revolution, including FMC corp and Sociedad Quimica Y Minera (SQM). Next up, globally renowned economist and editor of the GloomBoomDoom report, Dr. Marc Faber returns with his outlook on the financial markets for 2018.

Due to excessive expansion, of central bank balance sheets, global equities prices may be overextended as robust economic conditions are heavily dependent on inflated asset prices, including real estate and cryptos. Investors will turn away from the bubble markets to the precious metals, which will likely be next to outperform competing asset classes.

Although the Bitcoin mania reached a fevered pitch recently, approaching a total market cap for of $1 trillion (entire sector), Dr. Faber suggests that cryptos could continue to gain popularity after the current correction and increase another 20 fold to $10 trillion, rivaling the $7 trillion gold market, due in part to the limited supply of the top digital coins (figure 1.1.). Case in point, during the month long Bitcoin correction, Ethereum, arguably the silver to Bitcoin's gold, advanced over 100%, offsetting much of the selling - sector rotation is oftentimes viewed as a sign of bull market indication.

The guest / host concur, investment portfolio diversification is key to navigating through record market volatility and impending bubble implosions. Dr. Faber finds cash the most neglected asset class; holding currency could yield the gun powder necessary to procure discounted investment assets, following imminent price plunges.

According to Hugh Smith, "The core narrative of the Status Quo is that nothing fundamental needs to be changed: all the problems can be solved with more ‘free money’ (borrowed from the future at low rates of interest) and a few policy tweaks such as Universal Basic Income.

This core narrative is false: everything needs to change, from the bottom up. And that of course terrifies those gorging at the trough of status quo wealth and power."

Hugh Smith then discusses the theories of Peter Turchin. Peter Turchin is a Russian-American scientist, specializing in cultural evolution and the statistical analysis of the dynamics of historical societies.

His 2016 book Ages of Discord explains why we should be worried about the current course taken by American society and how we can use history to plan a better future. According to Turchin, "something happened to American society during the 1970s. Several previously positive social, economic, and political trends suddenly reversed their direction."

Turchin further explains that, "there were two periods in American history that were remarkably free of political violence: the Era of Good Feelings (the 1820s) and the post-war prosperity of the 1950s, which I termed the Era of Good Feelings II. After the quiet 1950s, however, incidents of political violence again became more frequent and now we may be in the middle of another wave of sociopolitical instability.

Waves of sociopolitical instability are characterized by:

1. An over-supply of labor that suppresses real (inflation-adjusted) wages

2. An overproduction of essentially parasitic Elites

3. A deterioration in central state finances (over-indebtedness, decline in tax revenues, increase in state dependents, fiscal burdens of war, etc.)"

I love the expression of "overproduction of essentially parasitic elites," which includes an oversupply of bureaucrats.

Fortunately, The pace of new regulation has visibly slowed in the Trump administration. A search of OMB’s database reveals that, between January and December 2017, the Office of Information and Regulatory Affairs concluded review of 21 ‘economically significant’ regulations - those with impacts (costs or benefits) expected to be $100 million or more in a year. There are indeed far fewer rules than previous presidents have issued in their first years.

The most impressive part is that some of these "significant" rules are actually designed to reduce red tape.

The S&P 500 has made history on a seemingly weekly basis with its record highs, but this unprecedented feat is about longevity. The index has gone for over 400 days without a 5% pullback, putting it at the longest streak on record, dating back to 1929, an infamous year no doubt.

But as Valerius observed in the first century A.D. "The divine wrath is slow indeed in vengeance, but it makes up for its tardiness by the severity of the punishment."

The Indian market may correct by 20-30 per cent, but it is attractive to stay invested in the country for long-term, said Marc Faber, editor & publisher of “The Gloom, Boom & Doom Report in an exclusive interview with Zee Business.

Faber also pointed out that India has the potential to become the second or third largest economy in the world. Edited excerpts:

Your thoughts on Indian budget and its impact on market?

Indian budget has been a mixed bag. I don't think stock market in India has fallen just on account of Budget. I think other factors are at play too.

What is your take on re-introduction of long-term capital gains (LTCG) tax in India?

I am against any kind of tax, be it LTCG, STCG, excise duty, or Value added tax (VAT). I think one should try to keep the government as small as possible. Best way to keep the government small is not increasing taxation, because the more money you give to the government, the bigger it will grow to be.

Do you believe the correction in India will prolong?

Everybody says it's a correction, but it's a premature statement. We don't know yet. It may be a correction of 5 per cent, 10 per cent or even 20 per cent, but it could also be a beginning of something more serious that may pull down the market much more.

What is the probability of that?

In US, a bull market started essentially nine years ago in March 2009. We are up close to 4 times since then, and in the last two years we never had a correction of more than 5 per cent. After these conditions, it is not unlikely that the market will face some tough time. Market may decline by 40 per cent. I'm not saying it will happen. I say it could happen.

Do you suspect globally markets may lighten up a bit and lead to adversely impact India?

Indian markets have now the yields removed. I had said two years ago that Indian markets will outperform US markets over the next 10 years. Two years are gone. But it doesn't mean that US markets can't have a significant correction. In 1987, we have had a 40% correction, followed by recession, then market continued to go up until 2000. My sense is we had a nirvana condition for financial assets over the last 8-9 years. Bonds, stocks and practically every sector has rallied. Dollar was firm. All these conditions will change. It will be more challenging for investors.

In the case of India, it has had a big rally, and a correction is overdue. But it's attractive to stay in India for long-term. India has the potential to become the second or third largest economy in the world, but at the same time, the benchmark may dip by 20-30 per cent but there will be shares that will move up.

If indeed market corrects by 20-30% in India, within EM basket, where will you place India?

A year ago, my top pick was Vietnam, but now it is also due a significant correction.

Your question is not easy to answer. Markets world over are being manipulated by central banks keeping interest rates low. In India, RBI's relatively tight monetary policy has resulted into rupee being strong and stable against dollar over the last two years. The RBI deserves some positive marks. I believe Indian economy may not be super healthy, but compared to others, it's a reasonably good bet to own.